Is the Storage in Big Data Market a Strategic Investment Choice for 2025–2033 ?

Storage in Big Data Market – Research Report (2025–2033) delivers a comprehensive analysis of the industry’s growth trajectory, with a balanced focus on key components: historical trends (20%), current market dynamics (25%), and essential metrics including production costs (10%), market valuation (15%), and growth rates (10%)—collectively offering a 360-degree view of the market landscape. Innovations in Storage in Big Data Market Size, Share, Growth, and Industry Analysis, By Type (Hardware,Software,Service), By Application (BFSI,IT and Telecommunications,Transportation,Logistics & Retail,Healthcare and Medical,Others), Regional Insights and Forecast to 2033 are driving transformative changes, setting new benchmarks, and reshaping customer expectations.

These advancements are projected to fuel substantial market expansion, with the industry expected to grow at a CAGR of 11.3% from 2025 to 2033.

Our in-depth report—spanning over 103 Pages delivers a powerful toolkit of insights: exclusive insights (20%), critical statistics (25%), emerging trends (30%), and a detailed competitive landscape (25%), helping you navigate complexities and seize opportunities in the Information & Technology sector.

Global Storage in Big Data Market size is forecasted to be worth USD 23499.45 million in 2024, expected to achieve USD 61590.56 million by 2033 with a CAGR of 11.3%.

The Storage in Big Data market is projected to experience robust growth from 2025 to 2033, propelled by the strong performance in 2024 and strategic innovations led by key industry players. The leading key players in the Storage in Big Data market include:

- Conagra Brands

- General Mills

- Hormel Foods

- Newman’s Own

- The Whitewave Foods Company

- AMCON

- Amy’s Kitchen

- Clif Bar & Company

- Dean Foods

- Frito-Lay

- Hain Celestial Group

- Organic Valle

Request a Sample Copy @ https://www.marketgrowthreports.com/enquiry/request-sample/103157

Emerging Storage in Big Data market leaders are poised to drive growth across several regions in 2025, with North America (United States, Canada, and Mexico) accounting for approximately 25% of the market share, followed by Europe (Germany, UK, France, Italy, Russia, and Turkey) at around 22%, and Asia-Pacific (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Malaysia, and Vietnam) leading with nearly 35%. Meanwhile, South America (Brazil, Argentina, and Colombia) contributes about 10%, and the Middle East & Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South Africa) make up the remaining 8%.

Storage in Big Data Market Trends

The Storage in Big Data Market is undergoing significant transformation, fueled by technological advancements and rising data dependency across all sectors. One of the most dominant trends is the integration of cloud-native storage systems. In 2024, more than 60% of organizations adopted hybrid or multi-cloud strategies for storing and managing big data. This has led to rapid development in cloud storage services offering high scalability, low maintenance, and cost efficiency.

Another major trend is the rise of edge storage solutions. With more than 30 billion IoT-connected devices globally, enterprises are increasingly deploying edge storage to handle localized data processing and reduce network latency. In the industrial sector, edge storage adoption rose by 28% in the past year, allowing companies to gain insights at the source of data generation. AI-powered storage optimization is also gaining momentum. Intelligent storage systems embedded with machine learning algorithms are capable of predicting storage failures, optimizing performance, and automating tiered data storage. Around 47% of large enterprises have integrated AI-based storage analytics to enhance storage efficiency and resource utilization.

Software-defined storage (SDS) has become a preferred choice for businesses aiming for flexibility and vendor-agnostic storage architecture. In 2024, SDS deployments increased by 33% among mid to large enterprises. SDS systems offer better scalability and centralized control, making them ideal for managing diverse big data workloads. Furthermore, the use of data lakes is increasing in organizations that need to store raw, unstructured data for future analytics. Over 55% of data-centric enterprises have adopted data lakes on cloud infrastructure to handle heterogeneous data sources such as logs, images, and IoT feeds.

Security is another trend shaping the market. As data breaches continue to rise, secure storage practices like encryption-at-rest, secure access control, and blockchain-based data integrity checks are becoming standard features. More than 70% of enterprises now prioritize end-to-end encryption and compliance with data protection laws such as GDPR and HIPAA when evaluating storage vendors. Lastly, the demand for green data storage centers has surged. With data centers accounting for approximately 3% of global electricity consumption, enterprises are increasingly shifting to eco-friendly storage infrastructure. In 2024, over 40% of new data storage facilities integrated energy-efficient cooling systems and renewable power sources.

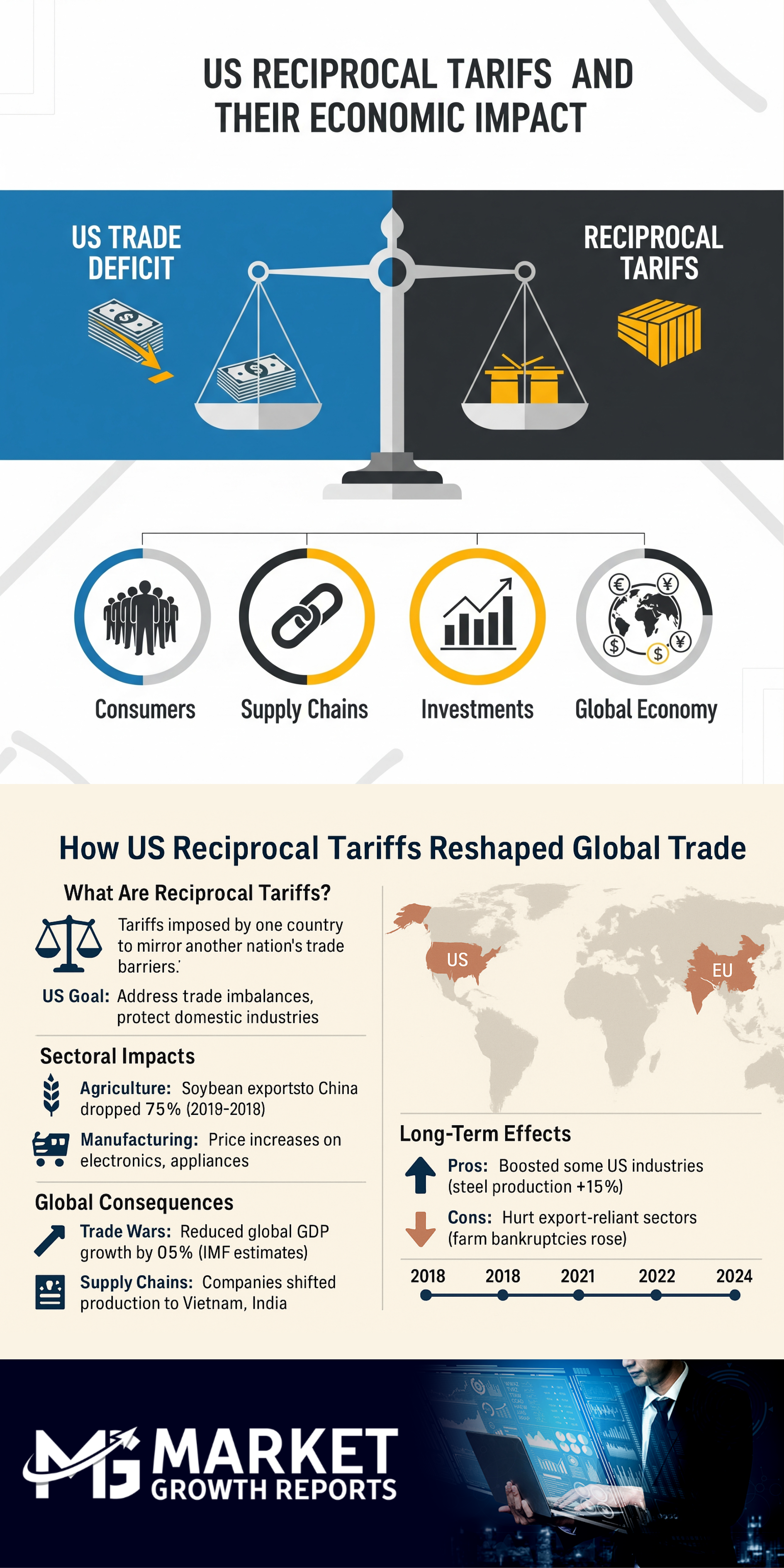

United States Tariffs: A Strategic Shift in Global Trade

In 2025, the U.S. implemented reciprocal tariffs on 70 countries under Executive Order 14257. These tariffs, which range from 10% to 50%, were designed to address trade imbalances and protect domestic industries. For example, tariffs of 35% were applied to Canadian goods, 50% to Brazilian imports, and 25% to key products from India, with other rates on imports from countries like Taiwan and Switzerland.

The immediate economic impact has been significant. The U.S. trade deficit, which was around $900 billion in recent years, is expected to decrease. However, retaliatory tariffs from other countries have led to a nearly 15% decline in U.S. agricultural exports, particularly soybeans, corn, and meat products.

U.S. manufacturing industries have seen input costs increase by up to 12%, and supply chain delays have extended lead times by 20%. The technology sector, which relies heavily on global supply chains, has experienced cost inflation of 8-10%, which has negatively affected production margins.

The combined effect of these tariffs and COVID-19-related disruptions has contributed to an overall slowdown in global GDP growth by approximately 0.5% annually since 2020. Emerging and developing economies are also vulnerable, as new trade barriers restrict their access to key export markets.

While the U.S. aims to reduce its trade deficit, major surplus economies like the EU and China may be pressured to adjust their domestic economic policies. The tariffs have also prompted legal challenges and concerns about their long-term effectiveness. The World Trade Organization (WTO) is facing increasing pressure to address the evolving global trade environment, with some questioning its role and effectiveness.

About Us: Market Growth Reports is a unique organization that offers expert analysis and accurate data-based market intelligence, aiding companies of all shapes and sizes to make well-informed decisions. We tailor inventive solutions for our clients, helping them tackle any challenges that are likely to emerge from time to time and affect their businesses.